Venmo vs Cash App vs Zelle: which to use to get paid back

By Mitch R, Tab Tender Team · 3 min read · Updated June 3, 2026

Use whichever app the payer already has: Venmo for the widest reach, Cash App for quick $cashtag sends, and Zelle to move money bank-to-bank with no separate app. Outside the US, PayPal, Wise, or Revolut.

Once you've worked out who owes what, you still have to actually move the money. In the US that almost always means Venmo, Cash App, or Zelle. They look similar but behave differently — here's how to choose.

On this page

The three big options

Venmo and Cash App are dedicated peer-to-peer payment apps with their own balances and social features. Zelle is different: it's built into most US banking apps and moves money directly between bank accounts. All three are free for standard personal transfers; the differences are in speed, where the money lands, and who already uses them.

| Venmo | Cash App | Zelle | |

|---|---|---|---|

| Money lands in | Venmo balance | Cash App balance | Your bank account |

| Standard transfer | 1–3 days (free) | 1–3 days (free) | Minutes |

| Instant transfer | Small fee | Small fee | n/a (already instant) |

| Separate app needed | Yes | Yes | No — built into banks |

| Identifier | @username | $cashtag | Phone / email |

| Best for | Widest reach | Quick sends | Bank-to-bank, no app |

Venmo

- Most widely used for splitting bills among friends, so the person paying you probably already has it.

- Money lands in your Venmo balance; a standard transfer to your bank is free but takes 1–3 days (instant transfers carry a fee).

- Easy to request money and add a note, which helps everyone remember what the payment was for.

Cash App

- Simple, popular, and quick to send with a $cashtag instead of a phone number.

- Like Venmo, funds sit in a Cash App balance; standard cash-out to a bank is free, instant cash-out has a fee.

- Strong in some regions and social circles — worth offering if your group leans toward it.

Zelle

- Moves money bank-to-bank, usually within minutes, with no separate app to fund or cash out.

- No balance to manage — the money just shows up in your checking account.

- Only works if both people's banks support Zelle, and there's no universal payment link, so you typically share your phone or email and the sender pastes it into their own bank app.

Which should you use?

Use whatever the person paying you already has — friction kills repayment. In practice that means offering more than one option. A good default is to list your Venmo and Cash App handles and your Zelle identifier, and let each person pick.

If you want the money straight into your bank with no cash-out step, Zelle wins. If you want the broadest reach and easy requests, Venmo is the safe pick.

Paying back outside the US: PayPal, Wise, and Revolut

Venmo, Cash App, and Zelle are US-only. If you or the people paying you are abroad, the common options are PayPal (almost everywhere, with a PayPal.Me link that prefills the amount), Wise (low-cost cross-currency, paid via your Wisetag), and Revolut (popular across Europe, paid via your revolut.me link). Each has a shareable pay link, so the experience is much like Venmo's.

The same rule holds as in the US: offer whichever one the payer already uses. PayPal is the safest single default internationally; Wise and Revolut shine when you're splitting across currencies.

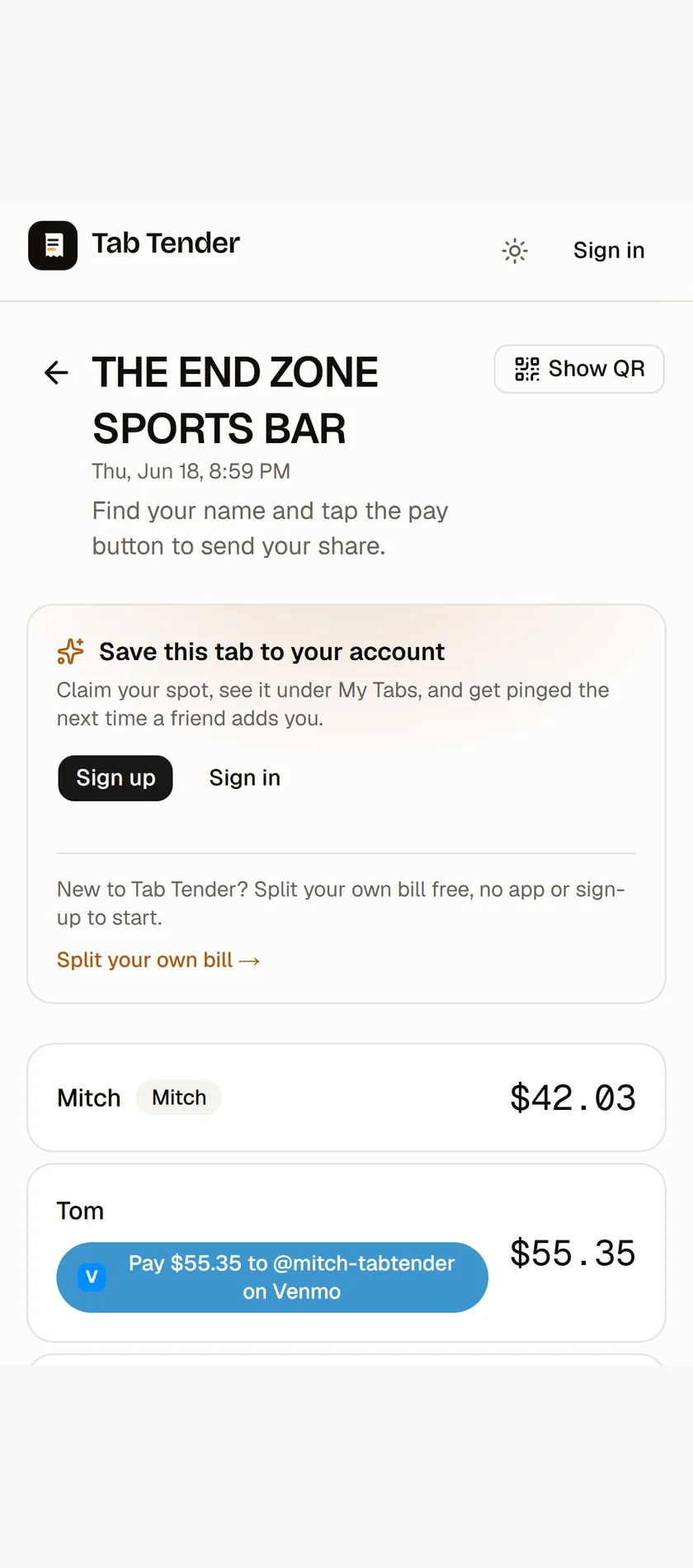

Make it one tap

Tab Tender turns each person's share into a ready-made pay link: tap to open Venmo, Cash App, or PayPal pre-filled with the exact amount, open your Wise or Revolut pay page, or tap to copy your Zelle identifier. Add your handles once in your profile and every shared tab generates the right link for each person automatically.